Nobody starts with a credit score. The frustrating part is that building credit often requires credit — a classic catch-22. The good news is that several credit cards are specifically designed to break that cycle, even if your credit file is completely empty.

Here’s what actually works for beginners.

Why Your First Card Matters More Than You Think

The credit card you start with shapes your credit profile for years. Choosing wrong — a card with predatory fees or a limit so low it’s useless — can make building credit harder, not easier.

Your first card should ideally have:

- Low or no annual fee

- Reports to all three major credit bureaus (Experian, Equifax, TransUnion)

- A reasonable credit limit

- A path to upgrade as your score improves

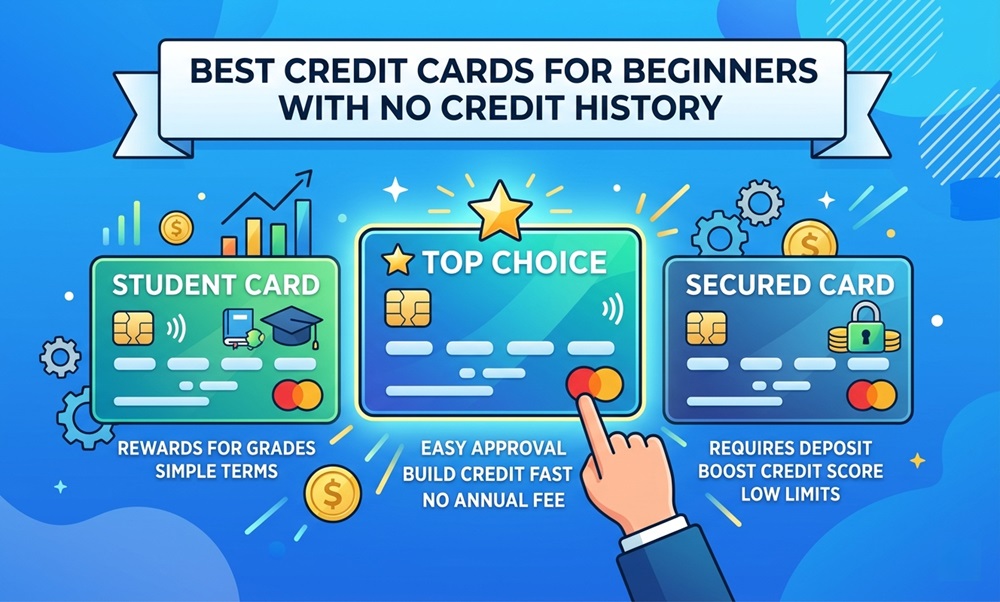

Best Credit Card Types for Beginners

1. Secured Credit Cards

You deposit money (usually $200–$500) as collateral, and that becomes your credit limit. The card works like a normal credit card — you spend, you pay, it reports to bureaus.

What to look for in a secured card:

- No annual fee (or low fee)

- Option to graduate to an unsecured card

- Reports to all three bureaus

2. Student Credit Cards

If you’re in college, student credit cards are the better option — they’re unsecured, don’t require a deposit, and often come with rewards. Issuers understand students are starting from zero.

3. Credit-Builder Cards from Fintechs

Cards like Chime Credit Builder or Self Visa link to your bank account and report your payments as credit activity. Low risk, no minimum deposit required.

Beginner Card Comparison

| Card Type | Deposit Required | Annual Fee | Credit Check | Best For |

|---|---|---|---|---|

| Secured card | Yes ($200+) | $0–$35 | Soft or none | Most beginners |

| Student card | No | Usually $0 | Soft pull | College students |

| Fintech builder | Minimal | $0–$25 | None | Very thin/no file |

| Store card | No | Varies | Yes | Brand loyalty users |

What to Actually Do in Your First 6 Months

- Use it for one small recurring charge — a streaming subscription, for example.

- Pay the full balance every single month — this is non-negotiable.

- Keep utilization under 30% — ideally under 10%.

- Don’t close it — length of credit history matters.

- Check your credit report at annualcreditreport.com after 90 days.

Common Mistakes to Avoid

- Applying to multiple cards at once — each hard inquiry dings your score.

- Only paying the minimum — interest charges add up fast and debt accumulates.

- Carrying a high balance — credit utilization above 30% hurts your score significantly.

- Missing a payment — a single 30-day late payment can drop your score by 60–110 points.

Expert Insight

The difference between a beginner who builds excellent credit in 12 months and one who struggles isn’t the card they chose — it’s behavior. Pick any solid beginner card, automate the full payment, and use it lightly. That formula works every time.

FAQs

Q: Can I get a credit card with absolutely no credit history? Yes. Secured cards and student cards are designed for exactly this situation.

Q: How long until I see my credit score? Most people get a FICO score after 3–6 months of reporting activity.

Q: Should I get a secured or student card? If you’re in college, get a student card — no deposit needed. Otherwise, start with a secured card.

Q: Will a secured card hurt my credit? No. It helps it — as long as you pay on time and keep balances low.

Q: When can I upgrade to a regular card? Typically after 6–12 months of responsible use. Many issuers do this automatically.

Conclusion

The best credit card for beginners is whichever one you’ll use responsibly. For most people, a no-annual-fee secured card is the safest, most accessible starting point. Use it lightly, pay it fully every month, and within a year you’ll have the credit foundation to qualify for nearly any card on the market.