Having no credit history isn’t the same as having bad credit — but it can feel just as frustrating when lenders treat it the same way. The good news is that building credit from zero is genuinely faster than repairing damaged credit. Done right, you can have a solid credit score within 6–12 months.

Here’s exactly how to do it.

Why No Credit History Is a Problem

Lenders use your credit history to assess risk. Without one, they have no data to work with. You’re invisible to the credit system — not bad, just unknown. Most lenders don’t like unknown.

The goal is to become “known” as quickly as possible, in a positive way.

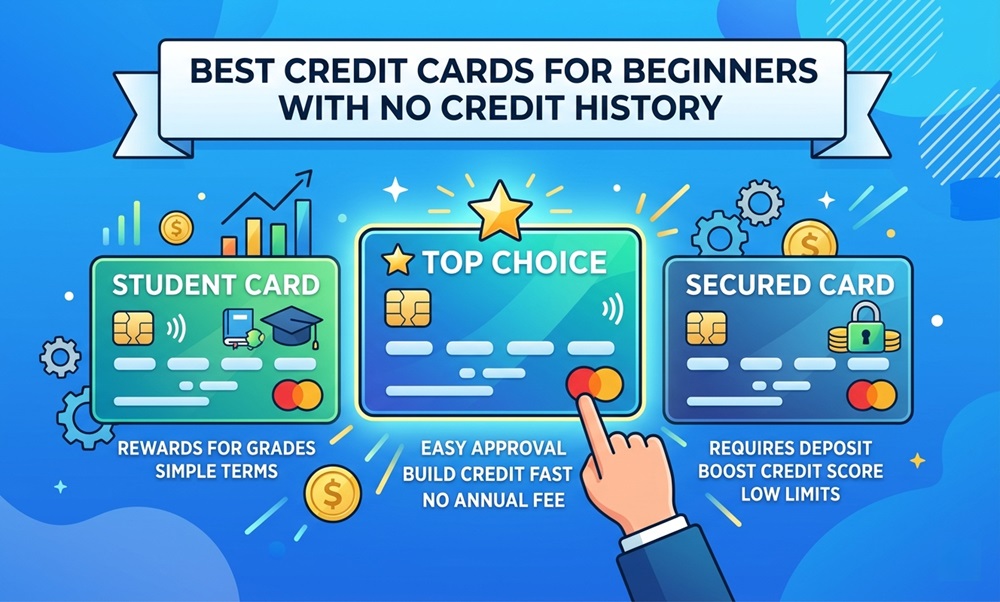

Step 1: Get a Credit Card Designed for Beginners

This is the fastest path. Specifically:

Option A — Secured Credit Card: Deposit $200–$500, get a card with that credit limit. Use it lightly, pay in full every month. Most major secured cards report to all three bureaus.

Option B — Student Credit Card: If you’re a college student, these require no deposit and are specifically designed for thin-file applicants.

Option C — Become an Authorized User: Ask a family member with good credit to add you to their existing account. Their account history can appear on your credit report immediately — even if you never use the card.

Step 2: Apply for a Credit-Builder Loan

Credit unions and some online lenders offer credit-builder loans specifically to help people establish credit. Here’s the unusual structure:

- You “borrow” $500–$1,500

- The money sits in a savings account while you make monthly payments

- At the end of the term, you receive the money

- Every on-time payment gets reported to the credit bureaus

It’s essentially forced savings that builds credit simultaneously. Self (formerly Self Lender) is the most well-known online version.

Step 3: Get Rent and Utility Payments Reported

Services like Experian Boost, Rent Reporters, and Credit Karma let you report utility bills and rent payments to credit bureaus. These aren’t traditionally included in credit reports, but adding them can help — especially when you have very little other history.

Note: Not all scoring models count rent reporting equally, but it doesn’t hurt, and it can give you a quick initial boost.

Step 4: Keep Utilization Below 30%

Once you have a credit card, your credit utilization ratio matters immediately. This is the percentage of your credit limit you’re using.

If your limit is $300, don’t carry a balance above $90. Ideally, stay under 10%.

Many beginners make the mistake of using their card heavily because they think activity builds credit faster. It doesn’t — responsible, low-utilization activity builds credit faster.

Step 5: Pay Every Bill On Time, Every Month

Payment history is the largest component of your credit score — roughly 35%. One missed payment can undo months of progress.

Set up autopay for the full statement balance if possible. If not, at least autopay the minimum and pay the rest manually.

Timeline: What to Expect

| Timeframe | Expected Progress |

|---|---|

| 0–1 month | Apply for card/credit-builder loan |

| 1–3 months | First credit score appears (FICO needs 6 months; VantageScore appears sooner) |

| 3–6 months | Score in the 580–640 range with consistent behavior |

| 6–12 months | Score in the 650–720+ range; eligible for many mainstream cards |

| 12–24 months | Strong profile; eligible for premium cards and favorable loan terms |

Common Mistakes to Avoid

- Applying to multiple products at once — Multiple hard inquiries look risky and slow your progress.

- Closing your first account early — Length of credit history matters. Keep it open.

- Carrying high balances to “look active” — Low utilization is better, not higher.

- Only using one credit-building tool — Combining a secured card + credit-builder loan + authorized user status accelerates results significantly.

Expert Insight

Being added as an authorized user on a parent’s or spouse’s account with a long, clean history is the fastest single action you can take to jumpstart credit. If the account has been open 10 years with no late payments, that history can appear on your credit report within 30–45 days — instantly giving you a foundation.

FAQs

Q: How long does it take to build credit from nothing? You can get a FICO score in about 6 months. A good score (670+) typically takes 12–18 months of consistent behavior.

Q: What credit score will I get after 6 months? With responsible use, most beginners land in the 600–660 range after 6 months. This is enough to qualify for unsecured credit cards and some personal loans.

Q: Does checking my own credit hurt my score? No. Checking your own credit is a “soft inquiry” and has no impact on your score.

Q: Can I build credit without a credit card? Yes — through credit-builder loans, rent reporting services, and being added as an authorized user.

Q: What’s the fastest way to get a 700 credit score from zero? Combine authorized user status (for immediate history), a secured card (for your own account), and a credit-builder loan (for installment history). Pay everything on time, keep utilization low. Most people reach 700 within 12–18 months with this approach.

Conclusion

Building credit from zero is a 6–18 month process, not a 6-week hack. But the steps are clear and the results are predictable: get a secured card or become an authorized user, add a credit-builder loan, keep balances low, and pay everything on time. Do those things consistently and you’ll have a solid credit foundation faster than most people expect.